Securities-based savings: Pillar 3a funds provide the following benefits

The private pension provision, known as the third pillar, supplements the government and employee benefits insurance. As an alternative to a pension account, securities-based savings are an attractive investment solution. Those who invest early in their pension provision improve the potential for larger returns by using Pillar 3a funds.

Pillar 3a: Pension account or securities-based savings?

Make private provisions for the future and close any pension gaps – that is the role of Pillar 3a. Choose between paying into a pension account and saving with securities. A Pillar 3a pension account is similar to a long-term bank account. You can contribute to your account at any time, flexibly, and without any pressure to save, up to the statutory maximum annual amount. You are also granted a preferential interest rate.

In the case of securities-based savings, however, you invest your retirement savings in a 3a fund. Even for small amounts, your participation in the financial markets is broadly diversified. While this is not without its risks, it often pays off over the long term: The returns mean that those who start investing early in securities are likely to have more money available when they retire than if they leave their assets in a pension account.

Securities-based savings explained in simple terms

Making provisions for the future while taking advantage of attractive potential returns – securities-based savings make it possible. Here's how it works.

Pillar 3a funds offer customized solutions

Various securities solutions are available depending on how much risk you assume and how long you want to invest your money. These differ primarily in terms of their equity component. The more equities there are in a fund, the higher the risk – but also the potential returns. Funds are managed actively or passively. With actively managed investments, professional portfolio managers work to optimize fund returns in the long term. Passive investments, by contrast, focus on a specific index and attempt to replicate it as closely as possible.

Always keep an eye on your 3a funds

Many people want to take advantage of potential returns but are put off by the fluctuation in the financial markets. Anyone looking to have round-the-clock control over their retirement savings can get an up-to-date and transparent overview of their portfolio on the Online & Mobile Banking, where they can also manage their own securities with just a few clicks. It’s quick and easy to optimize saving with securities should their personal needs or risk behavior change.

Whether a pension account or a pension securities account suits you best depends entirely on your personal circumstances. Credit Suisse experts will be happy to show you the various solutions and help you with the decision. Did you know you can switch from a Saving with securities – 3rd pillar to a Pension account – 3rd pillar, or vice versa, at any time?

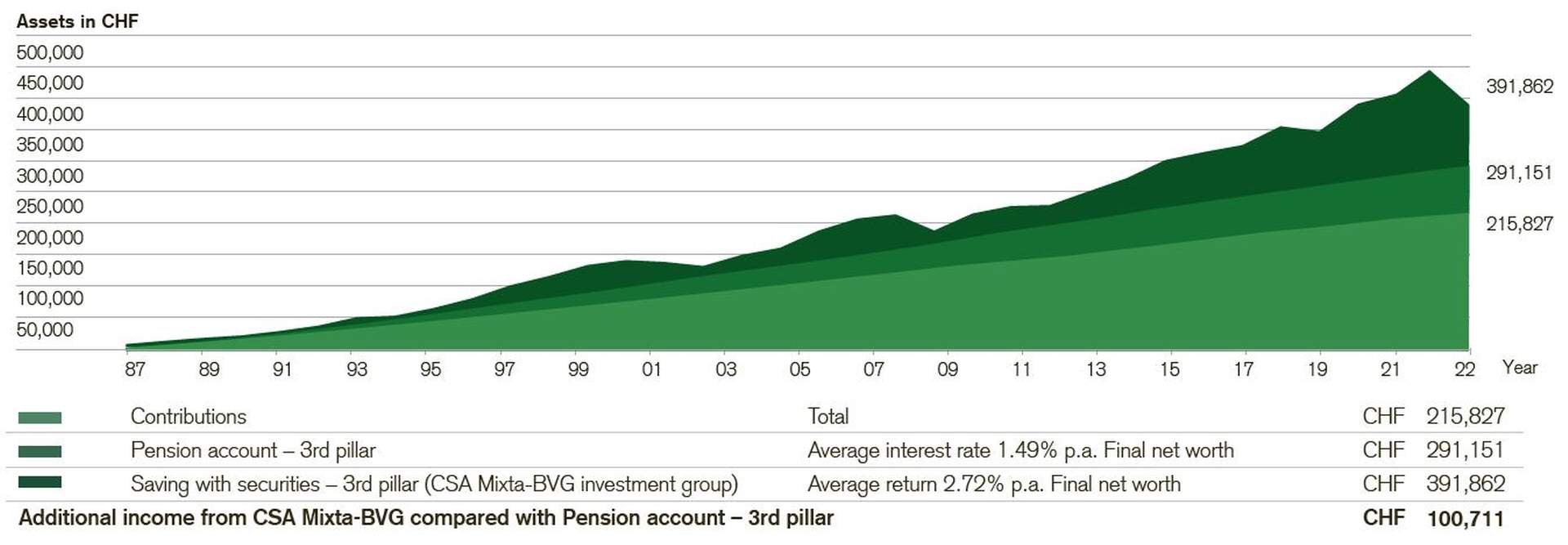

Return comparison between securities-based savings and a pension account

Both clients made the maximum contributions from January 1, 1987 through December 31, 2022 at the start of each year.

The client who opted for pension provision with securities (the CSA Mixta-BVG investment group in this example) achieved CHF 100,711 more in returns than the client who opted for the pension account.

Source: Credit Suisse

Historical performance and financial market scenarios are not reliable indicators of future performance.

Pillar 3a with an insurance company

You can also sign up for Pillar 3a with an insurance company. There are policies with securities and classic solutions without securities. In both cases, part of the payment is used for the insurance coverage and is consequently no longer available for retirement provision. As a result, you will have more money available after you retire if you have a pension solution held by a bank than if you take out life insurance.

With insurance, you are also entering into a long-standing contract, which can cost money to change. In order to stay flexible, we suggest saving up for your retirement with a bank and potentially taking out a separate risk policy with an insurance company for coverage in the event of death or disability.