Switzerland Press Release

Credit Suisse sees government spending as catalyst for Indian market in 2016; the impact of global weakness remains a concern

Neelkanth Mishra, Managing Director and India Equity Strategist at Credit Suisse points out the rising disconnect between the stock markets and the domestic economy. While hard indicators like oil and auto demand point to an economic recovery, popular stock market barometers like the Nifty and the BSE100 have been down over the past 12 months. There is also divergence between the broader market and the narrower indices: the BSE500 and the BSE200 have consistently outperformed the Nifty and the BSE100 in 2015. In fact, the "Next400", i.e. the 400 stocks in the BSE500 that are not in the BSE100, have together seen their market capitalization increase by 17% over the past 12 months, whereas the market capitalization for the BSE100 has fallen by 13%.

Global Linkages still pose risks in 2016

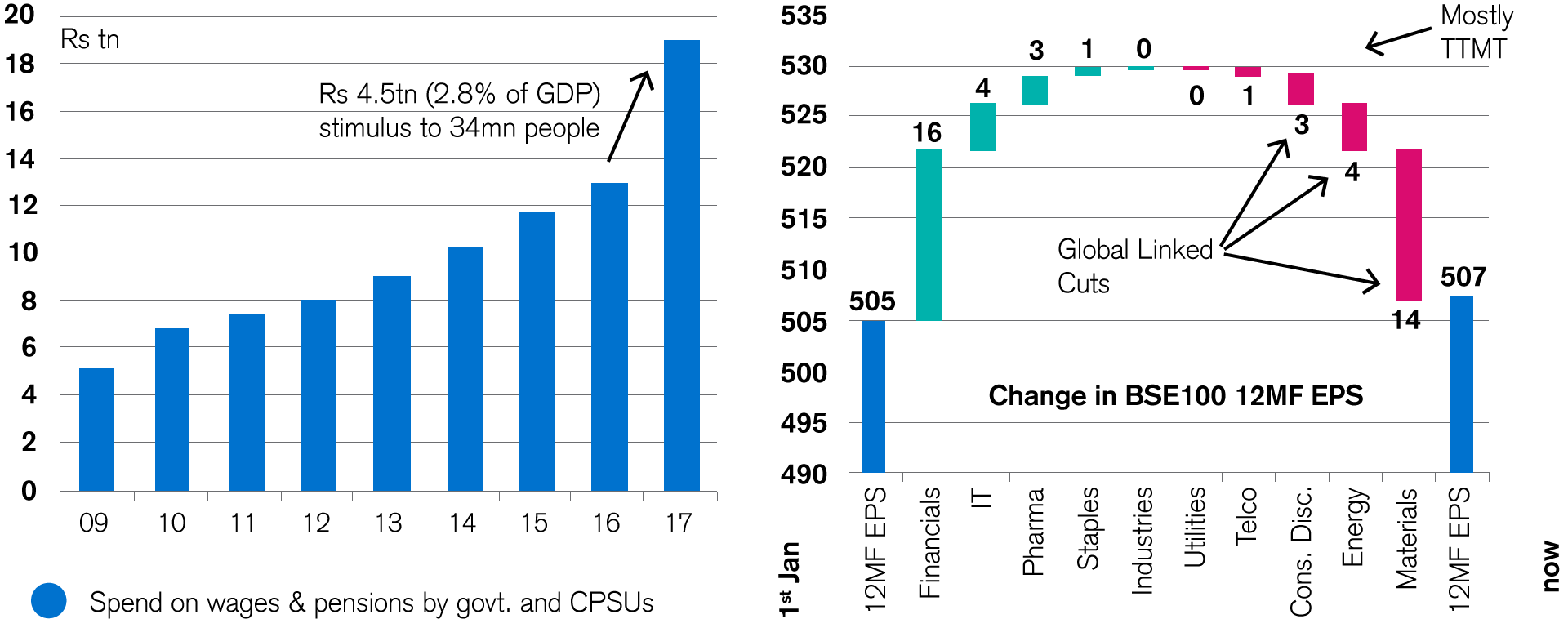

Mr. Mishra ascribes two reasons for this divergence: First of all, there is a significant global exposure among the larger stocks. More than half (53%) of the revenues for the BSE100 companies are linked fundamentally to what happens outside of India. Year to date, the reason the one-year forward earnings-per-share (EPS) for the BSE100 has not changed at all is that globally-linked earnings, such as for metals, energy and some global auto companies, have fallen materially. Even the remaining 47% includes banks that have worrying exposure to metal companies, and have therefore seen correction in their stock prices. The second reason is higher foreign ownership: FII equity outflows in the last three quarters have been the worst on record excluding the global financial crisis in 2008-09. As larger stocks have higher foreign ownership, the steady selling pressure hurts them the most.

These links are likely to continue to pressure Indian equity markets in 2016 as well. However, the impact should be slightly lower when it comes to earnings cuts. Throughout 2015, the pace of three-monthly EPS cuts for the Nifty/BSE100 indices was sustained at 3.5-5%, mainly because of high global linkages. This pace of earnings cuts offset the "roll forward" earnings growth of 3-4% a quarter, and hence hurt index performance.

Earnings cuts may persist, but at a slower pace

In 2016, the pace of earnings cuts may continue but should slow, for three reasons: Firstly, changes in index composition (global linkages are dropping as these companies become weaker and move out of the indices); secondly, absolute decline in commodity prices cannot be of the magnitude of 2015 (e.g. oil cannot fall USD50/bbl from here, and steel prices cannot fall USD200/t from here); and lastly, the pick-up in the domestic economy should help earnings forecasts for companies with local exposure.

Credit Suisse is advising investors to favour stocks of companies with local exposure, as the recovery is likely to strengthen in the new year. The pickup in government spending on roads and railways should translate into more downstream activity in the coming months boosting demand for labour, construction equipment as well as cement. In particular, the first 4-5 months of the calendar year should benefit from beneficial base effects. In the March quarter of 2015, a fiscal crunch caused a sharp slowdown in activity. With the fiscal numbers so far looking much better than last year, a similar slowdown in 2016 is unlikely.

Domestic government spending a catalyst; global linkages pose risk

Source: Budget Documents, 7th CPC Report, RAVE, Credit Suisse estimates

Pay Commission: A Rs4.5 trillion consumption stimulus

In the second half of the calendar year, Credit Suisse expects the 7th Central Pay Commission, likely to be implemented in June 2016, to trigger a massive process of cash transfer in the economy benefiting 34 million workers and pensioners. It starts with the central government, but is followed by state governments and Public Sector Units (PSUs). Together these add up to nearly 40% of India's active formal sector employment. A 27-29% salary hike could raise the comprehensive wage bill by INR 4.5-4.8 trillion over the next two years, with 75% of the increase in FY17. Rs4.5 trillion is 2.8% of FY17 GDP.

“We estimate that half the amount goes to about 80% of the beneficiaries that get increases of less than Rs10,000 per month and the remaining 6.5 million people will get an average of Rs24,000 per month extra in salary. Using the 2011-12 National Sample Survey Organisation Consumption survey, we find that incremental spending would be highest on food (mainly processed food), housing, transportation, jewellery, and entertainment,” said Mr. Mishra.

“The Pay Commission is an important milestone in the real-estate cycle in smaller towns. The Pay Commission can act as a significant broad-based stimulus, catalysing the dormant real-estate market in tier-2 and tier-3 towns, which in turn can be a significant source of labour demand, meaningfully impacting the broader economy,” he said.

Overall India's macroeconomic indicators such as balance of payments and inflation continue to be supportive, and it remains the fastest growing economy in both nominal and real terms. With 2014-16 earnings growth forecast of 13% CAGR, India ranks among the best markets globally. Price-earnings (P/E) multiples are also not high on a relative basis: Credit Suisse believes the with MSCI India's P/E premium to MSCI World (+11%) near ten-year lows, this is supportive of a 13-15% outperformance of the broader indices.